self selection bias. network is your net worth. so i choose my close friends wisely. with that said i have plenty of poor friends too. i do play ball at a ghetto park. i just dont bring them along when i hang with the rich folk. the ideal group of close friends is 4 imo. 5 is too tight in a car. lol

It doesn’t have to be anecdotal, as there is a lot of data available regarding net worth of people and their parents. I am pretty sure there is a clear statistical relationship between family net worth and income later in life. Don’t forget that rich parent also, in general, are better parents who provide a more stable upbringing, value academics, and are generally better role models for their kids. Financial support comes in explicit, but also indirect forms.

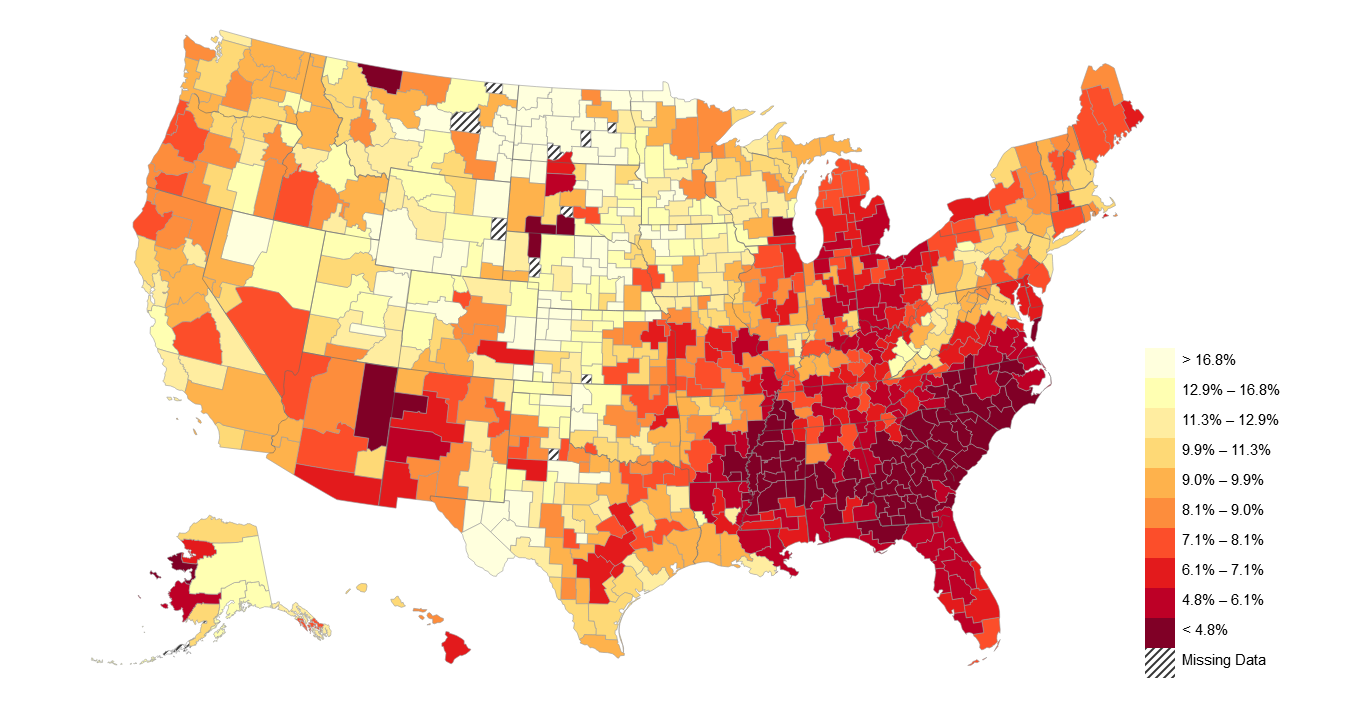

Absolute statements are usually inaccurate. To remove anecdotes, below is data on social mobility by state showing odds of reaching the top quintile of income given parents in the bottom quintile. This does not reflect the 1%, but it does show that there is economic mobility, although some may prefer more or less. In a completely fair world it would obviously be higher, but I don’t think anyone is under the misconception that Oliver Twist is the norm. If you find data on the 1%, please post it.

Also, saying the reason for the jump in the late 40s is inheritance is one thing. Saying inheritance includes anything parents paid for as well as quality of parenting is something else.

According to Investopedia

Household Income (2014)

Top 1% = $465,626+

Top 5% = $214,462+

Top 10% = 133,445

Median = $56,516

So all in all if you’re in a good profession like finance, med, law… then you’re doing a lot better than you think as long as you’re not drowning in debt.

This website gives income by age. I save about as well as I can without being a miser, so it’s what I use as a benchmark

https://dqydj.com/income-percentile-by-age-calculator/

I’ve moved up several percentiles recently without moving to a high cost of living area. I’m hoping that will help with the saving

I think we covered this in a more colorful post by Ohai (see link). In any case, dqydj’s figures are a bit high in my opinion. The 0.1% are probably smaller than they are projecting. Per Knight Frank and Credit Suisse, there are only ~40K and ~70K households in the US with $50M of NW. I don’t see that number tripling or doubling (depending on which source you use) to ~125K households dqydj estimates for the 0.1% when you go down to $43M of NW. Further, DB notes the 0.1% is $20M and up (that’s probably a bit low).

I’m also curious about the quality of people’s NWs. For example $10M of paper NW in a start-up is a lot different than $10M in more diversified stock/bond portfolio.

lets say you make 500k per year at 25 after your mba, and you make that much for 20 years and you retire at 45.

200k will go to tax per year. you need about 75k per year to maximize happiness. so you can prolly save 225k/year.

if you earn 8% per year on what you save for the next 20 years. at age 45, you’ll retire with 10m.

then you are in with the in crowd.

you can save even more if you mooch of your ‘friends’

Nery, where you come up with these scenarios? More realistically, you graduate MBA earning $170k with $100k in debt, and more likely 27 or 28 years old. Save maybe $50k a year. After say 5 years, there’s a chance you are making $500k, although most people won’t outside finance. You keep spending to live in a nice place like all your Ivy League friends. At 40, you’re house rich but cash poor. At 60, you have $5-$10 million sure, but you old by then. Where did life go? You might be divorced too, so you might be paying ransom money to some mean old bag, while also giving handouts to your moocher millennial parasitic adult kids.

Anyway, when I was thinking of doing MBA, I researched the #1 job offer at Harvard, which turned out to be around $560k. This presumably doesn’t count those tycoon kids who automatically run Samsung or something. This dude probably had a lot of existing experience though. There’s no reason to offer that to associate types. That’s the #1 guy - most are sub $200k at graduation.

haha lol i was being sardonic. i was trying to show that even a ridic income barely makes the cut. there is definitely something else you need to take make you worthy of the 1% title. to be in the 1% of earners at age 27 you need 134k.

but lets use your metrics.170k gross. is 110 net of taxes. deduct 75k for maximum utility. 35k/year saved. 3 years to pay debt 100k debt. so your start date is at age 30. lets assume 8% interest rate, at age 45 you will be worth 1.1m. way below the 10m needed to receive adulation

Most cases, it’ll take a few generations, nothing wrong with that. Won’t discourage me from trying to hit it in one.

If had to guess, I would say the bulk of those millionaires (like most millionaires) are small business owners that worked their a$$ of for 10-15 years – think medical professionals (with their own practice), contractors, lawyers, restaurant owners, franchise owners, and of course plumbers.

That’s it, going home to rethink my life with an icy beverage.

yes, that is exactly my experience (RE and investors also), as well as inheritance.

yup

Yes, most millionaires are business owners. This is the most common path for normal Americans to accumulate high net worth. For most people, the alternative is a job paying $50k to $70k, which provides a reasonable living in most places, but is not a path to capital accumulation.

Going back to the 1% ranges here though. I don’t think these ranges are unreasonable at all for someone who goes to a good school, and who receives only the implicit non-financial support of their parents through college and afterwards.

Age 30-34. $922k.

Age 35-39. $2m

Let’s say you attend some “top 10” ish school, and graduate at age 22 with $100k debt. After working at JP Morgan or BCG for 2 years, you’ve paid it off, and saved maybe $50k. Then, it’s business school. So, you’re 26 now with another $100k in debt. You pay that off in 1-2 years, since you’re earning $150k to $200k, and you might even be able to save $50k or so on top.

Now, you want to be worth $922k in 6 years when you will be 34 years old. Your earnings over this period might increase to say $300k to $350k at the end. This goal is ambitious but not unreasonable, and a lot of people seem to be in this situation.

That is not even the most efficient path. You could just work for Google and earn $150k out of college, going to $300k when you have 12 years of experience. You’d easily be a millionaire by 34.

For people who really only want to make money and have little passion for anything else, you can just work for GS or MS and you will probably be worth $3 million after 10 years of work. A couple hundred thousand dollars of debt will do little to change your wealth picture in this scenario.

Also note the limited risk in these scenarios. None of them involved real risk, like you would have if you started a business. All you would have needed would have been very good grades in school, good work ethic, and not doing anything stupid.

Long story short, if you’re already a top 1% in something (let’s say top 1% in school), you really can do this without much explicit financial assistance. The nurturing environment of a good household while growing up is another thing of course.

how do you pick your rich parents that care

^Yes doable, but still very challenging for most. As you noted, most of our discussion has not addressed potential risks such as job loss, voluntary time off, significant loss of principal in a recession, health issues, divorce, etc… These reasons and that it takes years to build up wealth, even on a high salary, are why most don’t make it to the top 1% by NW and even more so at an early age. To get there, you need something that truly builds a lot of equity. To your earlier point, this is why the 1% by NW is mostly reserved for the business owners.

300k is low end for 12 years engineering at Google, and i am talking single contributor role