Common dividends are _ always _ ignored in EPS calculations. We’re calculating how much we could pay in dividends (from net income), not whether we have actually paid it or not.

^ Also, the $100k that was deducted above is the pref share dividends, not the interest on the callable bonds.

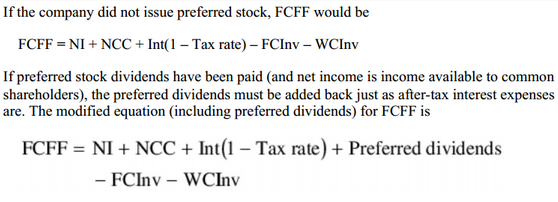

Net income already factors in the interest expense, but it does not factor in the pref dividends that the common shareholders do not have claim to (that is why they must be deducted).

basic EPS=(net income - preferred dividends)/weighted average common shares

It doesn’t matter. It’s still the bottom line, whether the NI or NIATCS.

I just wanted to throw it out that preferred dividends are sometimes included in the income statement, as part of the bottom line NI. If so, you do not adjust for them for the calculation of EPS, and add them back for the calculation of FCFF.

But this is probably outside the scope of a L1 candidate. So go with the material of the book.

It’s a hybrid security. Some of the preferred stocks are also cumulative. So they are an obligation in the sense that you cannot distribute earnings to shareholders before they get paid first. A mature company with PS in it’s capital structure that doesn’t dividends to CS will eventually see their market price take a hit. So in a sense, it’s not a contractual obligation, but it’s a critical one nonetheless. It’s not something you retain for added growth, since PS does not take advantage of earnings growth, or price appreciation. Hence why it does appear on the income statement for some firms, as it’s a form of obligation after paying interest.

For the small amount of companies that do have PS in their capital structure, some of them do include it as part of the bottom line. Haven’t I showed you the text book already?

This is just not a fact. Find me one real company that deducts preferred dividends from after-tax income to arrive at net income…since your above post would indicate you have come across companies that do this.