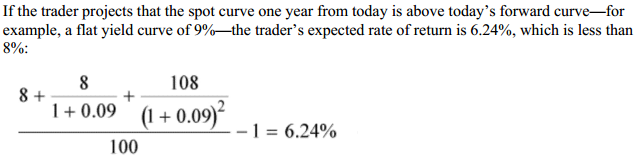

I don’t understand the following extract from the book. This is for a 3 year annual bond paying 8% coupon rate at a current market price of 100.

Do we not discount the first coupon by 1.09, second by 1.09^2? Why is the first $8 left undiscounted? Does this not assume that the trader buys the bond at the current market price and recieves 3 annual coupons in the future at a new rate of 9%?

Halp.