can someone throw some light around the hedging cost across the different available hedging option structures in the currency management and notably : 10-delta put, 10-delta call, 25-delta put, 25-delta call up to 25-delta risk reversal… I completely mess out when I try to understand which structure is cheaper than the other…which means which structure is further out of money…principle that I tend to apply is :

The larger the figure before “-delta” the more out of money —> the cheaper is but for sure it’s not working for Risk Reversal cause I found that a 10-delta Risk reversal is further OOM than a 25-delta risk reversal. Any help would be much appreciated here.

The values of deltas 10-Delta and 25-Delta are from 0.10 and 0.25 actual delta levels(ignoring signs).Moneyness is the criteria-More moneyness is offered at higher premium.The text mostly discusses puts-in Currency management,and in Single concentrated asset positions.

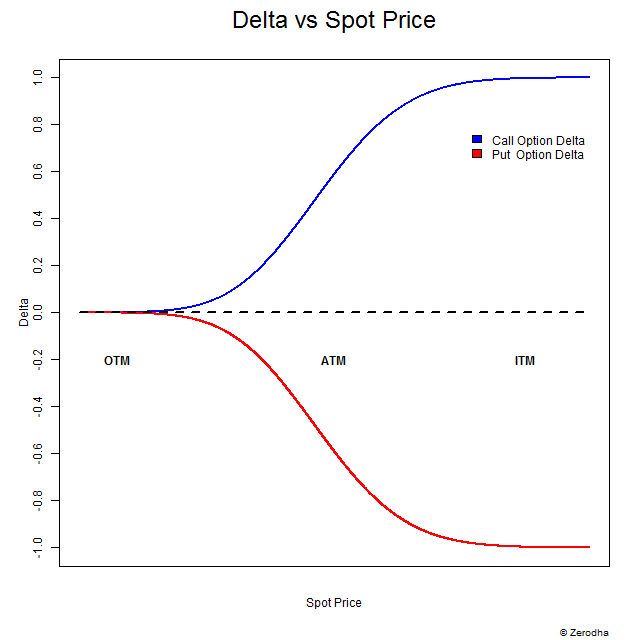

Thanks buddy but if I look at the greek graphs and if we assume that call value has a direct relationship with S (spot price) while put has inverse relationship with S…

CALL

a long 10-call which would cost less than a 25-delta call? (this is confirmed in the R28 currency mgt Example 7 solution 2…), thus the other way around for put…

PUT A 10-delta put would worth more than a 25-delta put which means that a 10-delta put cost more than a 25-delta put ?

"PUT A 10-delta put would worth more than a 25-delta put which means that a 10-delta put cost more than a 25-delta put ?"

It’s exactly the other way round. The higher the absolute delta of an option the higher the value of the option. No matter what type of option (call or put) it is. Please keep in mind that the delta of a put is always < 0 and the delta of call is always > 0. Therefore you have to use the absolute delta when comparing calls and puts.

The chart you quoted is quite misleading as the X axis corresponds to the moneyness of the option instead of the spot price (as indicated). For calls the option is in the money when spot price > strike, for puts it is when spot price < strike. This means for your chart: The blue line corresponds with higher spot prices (ITM for the blue line means that the spot price is ABOVE the strike), the red line with lower spot prices (ITM for the blue line means that the spot price is BELOW the strike).

There you find the chart you have posted as well as the delta of a call and a put in dependance on the spot price. I recommend to refer to these charts instead of the OTM/ATM/ITM chart.