Is CFA wrong because the equation(8) is for ERROR TERMS not RESIDUALS?

One assumes the residuals have an expected value of 0, so the variance is just the squared residual and one further assumes that the squared residual is some constant.

I mean RESIDUAL differs ERROR TERM

The CFA text is not very good at making the distriction between “residuals” and “error term”. It is a topic that is ignored.

1 Like

I believe the point they are making is that residuals and error term are not the same thing.

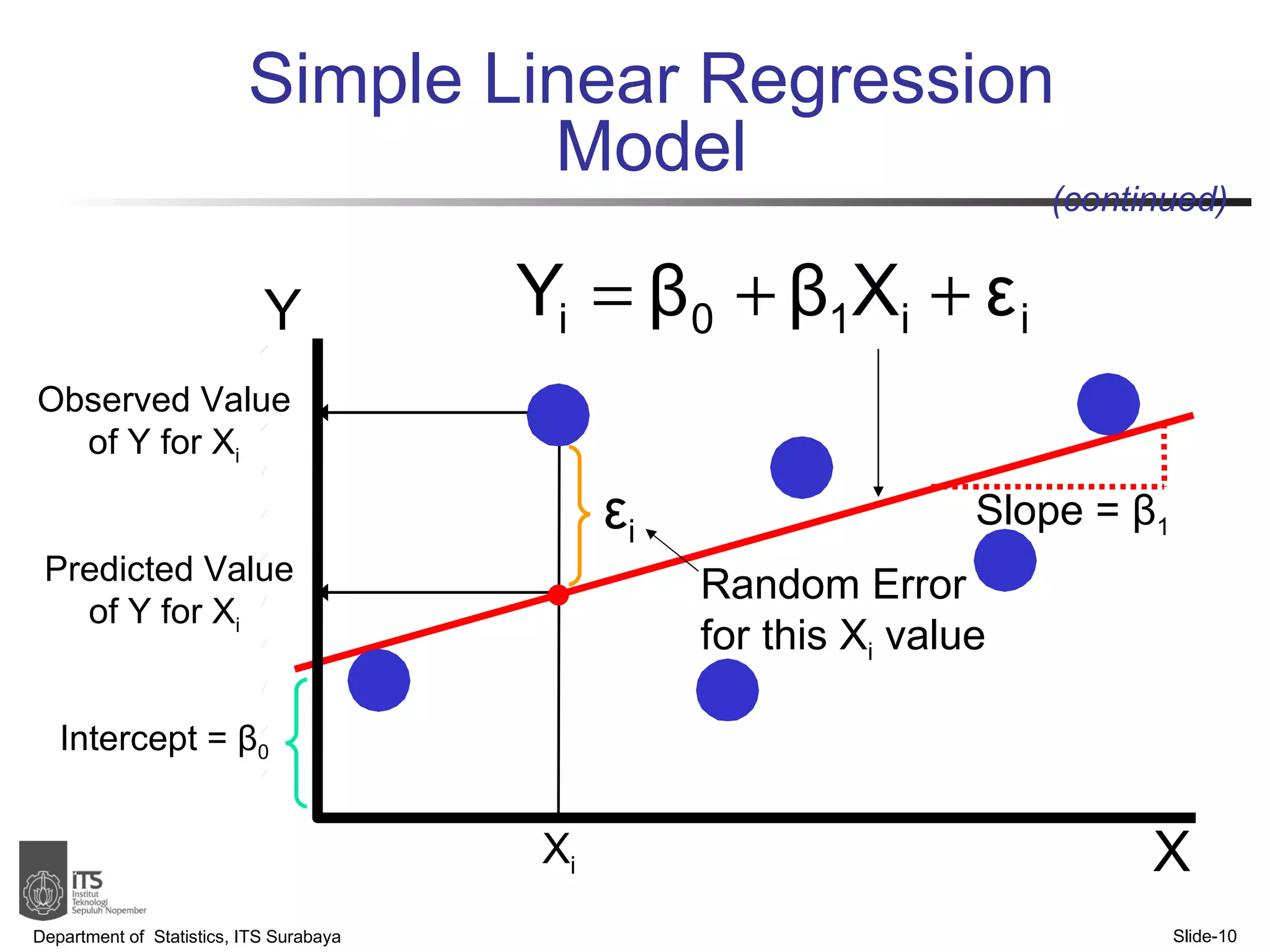

In the graph you show if Bo and B1 and “predicted” values rather than “actual values” then I believe the “e” term is not the error term but the “residual”

The residual is the difference between the predicted value and the observation. The error term - usuallly unknowable - is the difference between the “true value” and the observation.

If we use a sample to predict a relationship for a population we “predicting” the intercept and slope variables for the population. The difference between “predicted” and the observed is a residual not an error term.

1 Like

We called it both when I was in statz class back in the day. ![]()

for simplicity, residual is calculated based on SAMPLE DATA and error term is calculated based on POPULATION DATA.

OK, I will now incorporate “disturbance term” in my statz vocab!! ![]()