but thats under the assumption that oil isnt volatile. Oil hit 145 bucks in mid 2008, then went to $30 bucks by december of 2008. Down 80%. That’s 6 months, if u annualize that its even more ridic. then 1 year later in 2009 it hit 80 bucks. Up 250%. oil is friggin nuts.

u’ll see the same price change in 1996-2000. when global growth slowed due to the asian crisis, but us dominated.

and also. recessions hit when oil is at all time highs, not when oil is at all time lows. got it from cornerstone macro.

Put a big fat short on the market at 11:30 EST, money. Going to keep it on thru the Fed meeting.

What was with that 1.4% phony rebound? This reminds me of subprime in that people think “oh, that was crazy, but now it’s over”. It’s not over until all the leveraged high-cost fools go bankrupt, or until the damage becomes fully understood and priced in (which it currently is not).

Like I mentioned in a thread a few months ago, oil’s downfall will shift wealth in Canada from the West to the East. Ontario/Quebec will be the biggest winners. The loss in transfer payments will be outweighed by industries benefiting from more money in consumer pockets, and exporters and tourism benefiting from a lower dollar.

The global recession will not hit both regions equally.

Not sure who the manufacturing sector of Ontario will be selling to in a global recession. Further, the low dollar will just postpone any productivity investments. A recession or lower dollar doesn’t fix Ontario’s horrendous cost structure, high energy costs, unions and high taxes. This recession will slam all provinces.

To their biggest trading partner, the USA, which will be the cleanest shirt in a world with many dirty shirts. The East will be in recession while the West will be in depression. That’s where the difference lies. And when the economy trickles back up, I don’t expect there to be a bubble in resources due to a more balanced supply/demand structure than we’ve seen in the past decade. A bit like we experienced in the 90s where the economy was booming and resource prices were contained.

Let’s see how innovative and diversified Western Canada’s economy is with a sustained downtrend on energy prices. It’s a question of time before the brain drain reverses and the Eastern boys comeback home.

^ Well, the west is more diversified than many give credit to. My point was broader though than Canada. If the USA is booming and importing millions of huge Fords from Oakville and flying in new Learjets from Montreal, then oil is not at $50. You can’t have a booming world economy with cheap oil. Equity markets seem to be reflecting my point of view these days.

Forecasting oil prices is a bit of a fool’s game. I don’t think the recent price moves make much sense, but maybe I’m just naive. The January '15 Brent contract is $61.50/bbl, but out a year (January 2016) it’s $68.28/bbl. Over the last couple of months the futures curve moved from backwardation to contango pretty aggressively. We saw this in the last major price swing in 2008-2009. I don’t know what the storage rates on oil tankers is, but there could be some money to be made storing crude on tankers and locking in higher prices a year-plus out.

Just my opinion, but if crude oil is $58-$60/bbl, I don’t see how some of these oil majors can replenish their reserves if these prices stick. Deepwater, oil sands, tight oil, LNG – this is where the growth is and the economics get quite challenging at current pricing. There are some pretty major companies whose finding and development costs have risen rather dramatically even in a high oil price environment (we may see downward reserve revisions w/ lower prices). Some companies have been spending billions upon billions and still having a hard time keeping their head above water on their reserve bases (booking new reserves to offset their production). When your proven reserve base has a ~12-13 year life, if you sit on your hands for too long (not investing to grow reserves) you could get in trouble fast. Cheapest way to acquire reserves now may be through acquisition but the bid-ask spread is probably quite large given market volatility.

If people are looking at buying E&P’s, be sure to buy quality. Some companies will promote that they are in popular plays (Bakken, Eagle Ford, Permian) but their acreage positions within those plays may suck. Some of their balance sheets suck, too and they may be F’ed. Oil prices are obviously volatile and can be irrational, so they can go lower. I don’t think current pricing is sustainable though (citing the costs to replace reserves) unless we’re going into a global recession. Just my opinion and I’ve been wrong before.

Yes. Immediately followed by disaster. This cycle will be shorter. We don’t have the household balance sheets this time to borrow out of the mess. Look at autos, the only way to sustain demand is huge negative equity 84 or 96 month loans. We are in a bubble in consumer spending. The growing bubble in 1999 was asset driven, different. That said, oil demand is fairly inelastic and prices will recover to kick the rest of the economy while its down, again, much like what followed 1999. Is oil a leading indicator? Perhaps.

Woke up Sat morning (Asia time), to a fat increase. Thank you fear and volatility!

This feels ugly thru next week. Who wants to go long and get caught again with news that oil has hit 50? Market has been at all time highs and investors wonder if it isn’t the top. Fed not raising rates won’t actually help the oil situation. Economic numbers won’t be great, they were will poor to avg, and won’t offset oil fears. Seems like a more downward pressure/possibilities than upward.

The bond market (where the smart money truly is) is a leading indicator. The yield curve inverted 7 times since the 1950’s and in all 7 cases, a recession followed in the next 5 to 16 months. The lone non signal was 1960. 7 out of 8 ain’t too shabby

Oil at $148 in the summer of 2008 mislead investors both in terms of economic expansion and inflation. Oil at an average price of $15 (inflation adjusted $24) in the 1990’s would have made investors following that indicator to miss out on the greatest bull run in US equities ever.

All that being said, I do believe in the Lost Generation and in a fairly low growth rate going forward for still another decade. Some regions will do relatively better than others under this scenario, which will translate in financial and human capital moving there.

Some say selling may continue as few participants are yet willing to call a bottom for markets.

But Badri suggested the crude price fall had been overdone. “The fundamentals should not lead to this dramatic reduction (in price),” he said in Arabic through an English interpreter.

He said only a small increase in supply had lead to a sharp drop in prices, adding: “I believe that speculation has entered strongly in deciding these prices.”

Asked if OPEC planned an emergency meeting before its next scheduled gathering in June, or a meeting with non-OPEC producers, Badri said such meetings would not have an effect on oil prices.

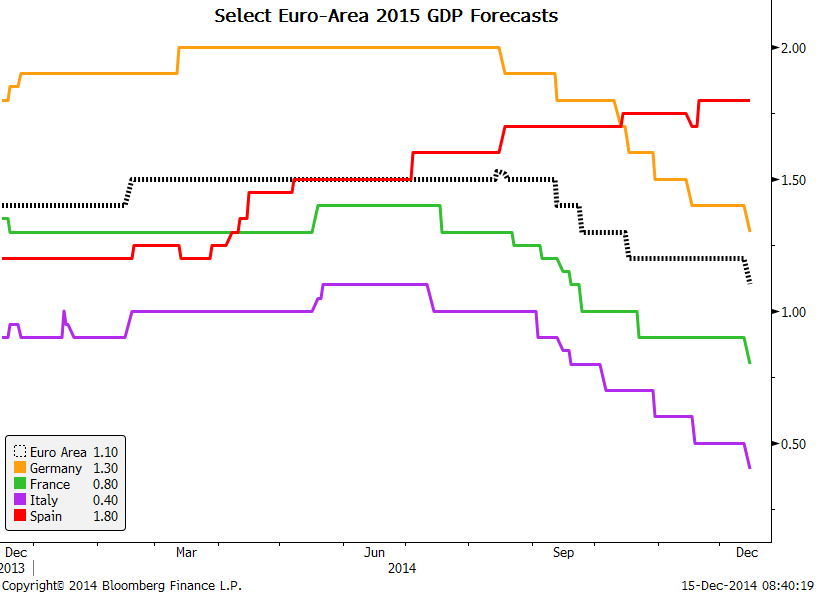

^ What exactly do they do in Italy anyway? I’m curious how real GDP growth and real GDP per capita growth differ when comparing the US and Eurozone. Sure the US has had more robust growth, but how much of that is population driven? Hmm…

I find it funny that the peons out here are all cheering lower gas prices, blissfully unaware that 2015 raises are going to be 0% in energy. Yay, I saved $5 which cost me thousands!

I’ve been diving into a company that has heavy investments in the eagle ford / bakken shale. They cut their production forecasts in their latest 10q but gave guidance on higher production forecasts in 2x15. Their p/cf is a little over 2 and qtr and their p ebitda is just shy of 3x. their balance sheet is well equiped to last when prices are low (i cant define a period though) and the street consensus have price targets well above the current market price (although these have been revised down by most).

My question for this group is, on average, what is the breakeven price at which the average shale production company can profit?

For more info, the company im considering is SM Energy

I’m curious how real GDP growth and real GDP per capita growth differ when comparing the US and Eurozone. Sure the US has had more robust growth, but how much of that is population driven? Hmm…

I’m curious how real GDP growth and real GDP per capita growth differ when comparing the US and Eurozone. Sure the US has had more robust growth, but how much of that is population driven? Hmm…