Why would anyone in Calgary ever cheer lower oil?

I’m also interested in this. To what degree will Bakken and other shale fields stay profitable at these levels?

I’m not an expert in this energy area, but it’s fairly clear a lot of leveraged high-cost producers are going to bite it next year if this sustains…

-------------------------- "Our oil forecast calls for a slowdown in US shale oil production which our North American Energy equity research team led by Brian Singer estimates will occur at $75/bbl WTI prices.

They estimate that the WTI oil price at which average wells in the Eagle Ford, Bakken and Permian Basin plays achieve an 11% IRR ranges between $70-$80/bbl. More importantly, they believe that funding gap constraints below $80/bbl WTI will ultimately drive the slowdown in production."

http://www.zerohedge.com/news/2014-10-29/why-75-most-important-number-us-economic-hope

Because 80% of the population (not just Calgary) is dumb as hell. Everyday when I drive past the pump, I cheer higher prices. And I don’t even work in energy. It affects home prices and wages for the whole city (and as I argued before, much of Canada, albeit more indirectly).

There is a considerable difference in the price at which you’d expend capex and the price at which an existing well can profitably operate. Its sustaining capex that is the problem. You could theoretically run most of these companies without new wells for a few years and show P&L profit, but the business would be gone as decline rates are so high in this game

Also have to keep in mind the majority of people (while being dumb) spend a large portion of their disposible income on gasoline. They’re already underemployed, largerly indebted and likely ignorant to the fact that demand creates higher prices but also more jobs.

For me personally, I don’t really care what happens in the short term. If anything this gives me an opportunity to buy some E&P assets of a stable corporation.

It’s coming but not yet.

I second what geo said.

I haven’t followed SM Energy, although have similar companies. I’m not too familiar with the area where they operate in the Eagle Ford, but their acreage in the Bakken is not attractive. In the Eagle Ford, the best drilling results are probably ~100 miles east of where SM is. So long story short, their crude oil-weighted acreage in the Bakken sucks and needs higher prices than average (Montana, Divide county and southern McKenzie county is not where you want to be in the Bakken) and in the Eagle Ford I don’t think they are getting a lot of true oil – its NGL’s, condensate and dry gas. I looked at their financials and their Eagle Ford production is only 17% crude oil. SM really isn’t much of a crude oil player; it’s mostly nat gas and NGL’s. For them to be more of an oil producer, they need high oil prices to make their Bakken acreage more economic.

Their capitalization is pretty good, which I’m guessing is why you’re interested in them. Just understand that they are 50% dry natural gas and their aceage positions in these popular plays is second-rate at best.

If you want quality in the U.S., EOG is the way to go. They are excellent.

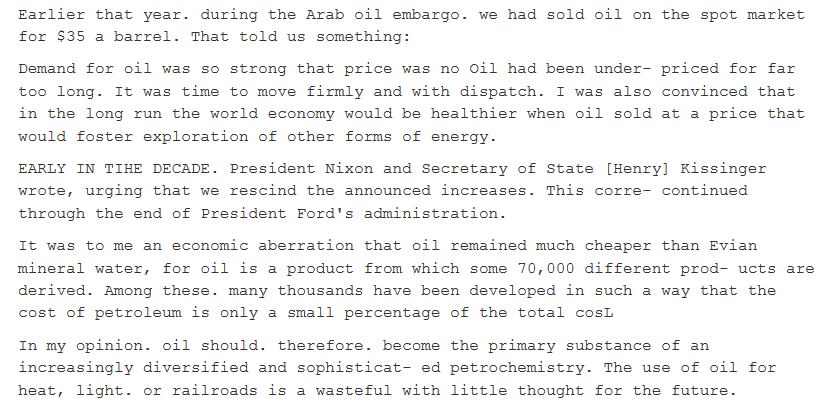

Funny thing an energy guy posted on Twitter today: Brent crude now selling for ~40% less than bottled mineral water in Britain’s supermarkets (20% less excluding VAT)

He then included this article from 1980:

good insight, can i ask where you attain your information from? I agree with EOG, this is on my watch list too

^ There’s a lot of good information you can obtain from individual companies, from investor events (presentations are often available under investor relations) and transcripts if you can’t attend. There’s dozens of smaller E&P’s out there you can analyze and derive your own info. I’ve spent a fair amount of time analyzing these companies for work. Regarding Bakken data, I believe Hess Corp. has a good slide or two in their analyst day presentation (page 34) last month that details some of the drilling results in the Bakken – maybe the best data I’ve seen publicly. The sweet spot of that play is right in eastern portion of McKenzie county. QEP Resources has a very fine acreage position there; unfortunately they also bought Permian acreage at the peak of the market and have some less attractive gas assets.

SM’s acreage in the Bakken isn’t good, and it doesn’t give them much access to the Three Forks formation below the Bakken that gives them more drilling opportunities. I don’t mean to trash SM or anything, it may end up being a good investment if the valuation is attractive enough.

Sorry about pumping EOG (I’ve brought them up before). I don’t own the stock or anything but they are just years ahead of the industry. Great operators and their financial health is good.

though i’m not 100% writing off the possibility of a recession, the oil price decline seems much more like a supply issue than a demand issue. it MAY be partly a demand issue, but it is CERTAINLY a supply issue.

look to 1985 as a case where a rapid decline in oil prices, due to lower demand (rapid improvement in fuel efficiency like we have seen over the past 5 years and other efficiencies) and ample supply, led to a 65% decline in oil prices and no global recession. in fact, the oil price decline in 1985 is likely part of the reason for such a strong period of economic growth between 1985 and 2000.

you fail to remember that OPEC could increase oil production by 2 million barrels a day within a few months and push prices to $20 for a couple of years, absorbing some lost production in North America and elsewhere, if it really wanted to. oil prices are not a good predictor of what is happening in the rest of the marketplace due to this possibility. because OPEC said they will not decrease to support prices, what’s stopping them from increasing production? if the Saudis really wanted to, they could probably increase production by 5 million barrels per day within a couple years if they allocated the capital towards it and made it a priority, and it would be profitable for them to do it!

geo. i like ya. and i need you to contemplate this reality b/c i’d rather not see you get killed thinking that oil will come back in the next year or so. i think it’s a real possibility that almost everyone has this one wrong and that we could be at $50 for several years. i know its difficult but there is a possibility that the age of oil and alberta is over, at least for a couple decades.

if you’re a disgruntled OPEC member and you want prices to be higher but the Saudis are saying no, you are inclined to increase production despite its effect on prices so long as your wells are profitable in order to maximize employment and reduce attempt to reduce your deficits. one of the best ways for Iran and other countries with low cost fields facing huge deficits to reduce their deficits will be to maximize employment (i.e. drill baby drill). this could easily be the start of a period of rising OPEC supply and stagnant oil demand.

http://en.wikipedia.org/wiki/1980s_oil_glut

http://www.macrotrends.net/1369/crude-oil-price-history-chart

^ I agree there is the possibility that oil may stick at these levels longer term, but I’m skeptical. The production in North America is not the same as in the 1980’s. US production falls off a cliff with a reduction in capex, which we are seeing. These decline rates did not exist in the 80’s and therefore you had legacy wells kept on stream as they had positive netbacks. I’m not increasing positions but I’m also not running scared. I’ve taken a hit sure, but this is a longer term cycle. Anyway, supply forecasts are level or lower versus a month ago. Its not like the market just woke up and realised the Bakken exists. So what’s changed from a bearish perspective? The demand forecast is revised downward, despite lower prices. That’s a very bearish signal globally beyond oil.

i still don’t really agree with the reduction in demand growth. aren’t the reductions just due to the reductions in the GDP growth of oil producing states, as per the IEA? the demand growth reductions are due to low oil prices not because of lower global GDP growth. remember that many oil producing states are terrible energy consumers and if their gdp declines, the world’s energy efficiency improves.

i don’t think you can claim a 4% decline in the S&P500 from its highs is a telling indicator about future global GDP growth. the S&P 500 ex-energy is very close to an all-time high.

i think that all else equal, if a decline in oil prices is mostly a shift in transfer payments between oil consuming nations and oil producing nations, world GDP expectations should adjust upwards as OPEC members will increase debt to finance current spending and/or increase production to finance some of current spending meanwhile any oil consumers, U.S., Europe, Japan, will see a boost to consumer demand.

Canada in particular will be a slight positive at best but capital flight could mean near-term pain. clearly the non-energy focused economies should improve, particularly those in Ontario and Quebec with minimal oil and gas exposure. though manufacturing may not come back in a big way, a reduction in capital investment toward energy and into technology and health care will assist these economies more than any others.

this is 1985 all over again. not 2008. that said, just because it resembles 1985, it doesn’t necessarily mean we should expect 15 years of rip-roaring equity markets but it should make us more constructive on the non-energy part of equity markets than in early 2014.

EDIT: what’s changed is that the odds of OPEC going from 30.5M/bbls/day to 32M/bbls/day over the next couple of years just went from 0.01% to 50% and those 1.5M/bbls/day are the most important barrels on the planet, and they’re fairly cheap to produce.

Agree with MLA. I think people are overestimating the demand destruction. Markets tend to work with a lag and the lower oil prices have yet to work their way into the economy in any meaningful way. As that happens I see that pushing up equity prices.

I can see Canadian Energy stocks disappointing generally in 2015 which would be a drag on the TSX. There will be some great buys in Canadian Energy but I think that might be a 2016 story. I could be wrong but I think demand for Energy will continue to grow and I’m of the opinion that we’ll see $100/bl again. When it will get there though I have no idea.

I’m with Matt in that overall, I’m constructive on the non-energy/materials part of the Equities. I think we still have a couple years left in this market before we pull back meaningfully and the decline in oil helps more than hurts in my opinion

The thing that doesn’t get talked about much in the media is that oilfields decline by approximately 4.5% annually (this is well documented by lots of research). So if daily oil production is 90 million barrels per day in 2014, it’ll be 86 million bpd in 2015 and 82.1 million bpd in 2016 without adding any new production. There just aren’t the low cost oilfields out there that haven’t already been brought on-line – new projects aren’t incentivized at oil in the mid $50’s. If world economic growth is around 1.5% and oil depletion is 4.5% annually, I just don’t see $50-$60/bbl sustained b/c we need new production to replace the depletion The world needs Alberta it if it’s going to grow. If we’re going into a global recession/depression it’s a different story, however.

I do think there has been a good deal of froth in North American production in recent years, though. I think this ‘correction’ is kind of needed to flush out some of this malinvestment going on.

I just saw a segment on the news on what’s going on in Whistler, BC. They are experiencing a mini boom. The lower dollar is bringing American tourists in droves and lower prices at the pump is bringing drivers in droves. They are already talking about the most profitable holiday season in ages. The transfer of wealth between industries is already happening.

CIBC just came out with a report that simply plagiarizes what I’ve been typing in this thread (well almost):

"Meanwhile, at that $70-per-barrel price, the hit to Alberta’s revenue could be $7 billion in 2015/16, while Saskatchewan, as well as Newfoundland and Labrador could each lose between $400 million and $700 million in revenue. The energy sector accounts for nearly 10 per cent of Canada’s GDP, “but in the oily corners of the country – Alberta, Newfoundland and Labrador, and Saskatchewan – that sector’s weighting is closer to 25-30 per cent.” “We staked out a much more positive view of Ontario’s relative growth prospects back in the summer as the U.S. economy accelerated and the (Canadian dollar) eased, and our conviction around that call has only grown,” the economists write. “In fact, Ontario could be poised to lead the country in real GDP growth in 2015, with Quebec likewise due for a notable acceleration.” Each $2 drop in crude prices shaves about a cent per litre from prices at the pump, the economists note. “So even if oil rebounds to average $70 next year, the savings could provide Canadians with the equivalent of a $10 billion boost to incomes.”

A shockingly good article here.

http://seekingalpha.com/article/2759495-what-is-saudi-arabia-thinking