Does anyone know why the below problem does not work using the sum product of active weights and active security returns? To be clear, using 0.15(10-8) - 0.10 (10-9) - 0.05 (5-6) = 0.25, but the correct answer is actually 1.05. Can anyone please explain?

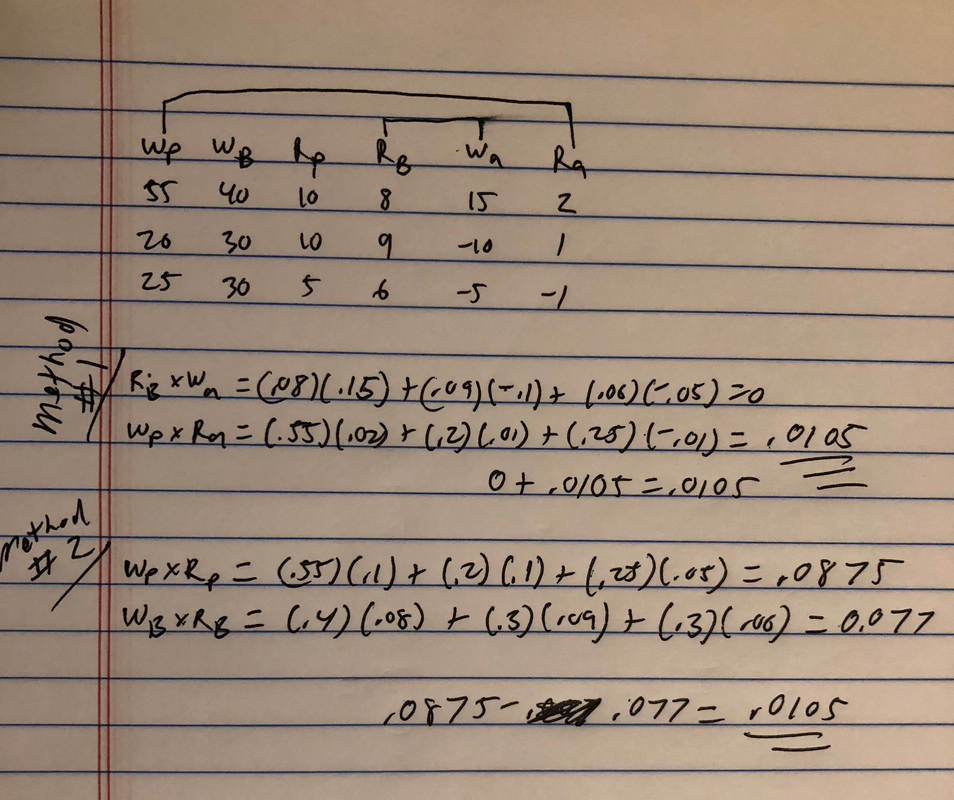

Consider the following asset class returns for calendar year 2016:

Asset class** Portfolio****Weight (%)BenchmarkWeight (%)PortfolioReturn (%)BenchmarkReturn (%)** Domestic equities 55 40 10 8 International equities 20 30 10 9 Bonds 25 30 5 6

What is the value added (or active return) for the managed portfolio?

- 0.25%

- 0.35%

- 1.05%